India has rapidly emerged as one of the world’s fastest-growing startup ecosystems. Every year, thousands of entrepreneurs, freelancers, and small business owners take the leap to start their own ventures across industries like technology, retail, finance, and services. While the enthusiasm is high, many first-time founders often overlook one of the most important steps of building a sustainable business - company registration.

Registering a company is much more than a legal formality. It establishes your business as a separate legal entity, gives it a distinct identity, and creates a strong foundation for future growth. A registered business enjoys greater credibility with clients, suppliers, and investors, and it also becomes easier to access loans, attract investment, and participate in government schemes. Without registration, businesses often struggle to open current accounts, sign legal contracts, or qualify for tax benefits.

The good news is that the company registration process in India has become completely online and highly streamlined. The Ministry of Corporate Affairs (MCA) has introduced the SPICe+ (Simplified Proforma for Incorporating Company Electronically Plus) form, which integrates name approval, incorporation, PAN, TAN, and even GST registration into one application. This has made the entire process faster, more transparent, and significantly less complicated than before.

Whether you plan to start as a Private Limited Company, Limited Liability Partnership (LLP), One Person Company (OPC), or another structure, understanding the requirements and process is critical. In this detailed guide, we will walk you through everything you need to know about company registration in India from choosing the right business structure to step-by-step registration, required documents, costs, compliance obligations, and frequently asked questions.

Get Your Company Registered

Contact Tax Rupees for all your Business Needs

Why Register a Company in India?

Many entrepreneurs in India begin their journey informally, but sooner or later they realize that operating without legal registration creates serious limitations. Registering your company is not just about fulfilling a government requirement; it is about building a strong foundation for long-term success. Here are the key reasons why registration is so important:

1. Separate Legal Identity

Once registered, your company is recognized as an independent legal entity separate from its owners or shareholders. This means the company itself can own assets, open a bank account, sign contracts, and even initiate or defend legal proceedings in its own name. For entrepreneurs, this distinction creates a clear boundary between personal identity and the business entity, which is critical for growth.

2. Limited Liability Protection

One of the biggest advantages of registering a company is limited liability. In sole proprietorships and partnerships, personal assets such as your house, car, or savings can be seized if the business incurs losses or debts. In a registered company, liability is restricted only to the capital invested in the business.

Example: If your Private Limited Company defaults on a loan of ₹20 lakh, your liability is limited to the shares you hold not your personal property or savings.

3. Investor and Loan Access

Most banks, NBFCs, and equity investors prefer working with registered businesses. Venture capitalists and angel investors, in particular, often refuse to fund unregistered entities. By registering your company, you increase your eligibility for loans, credit facilities, and funding opportunities, making it easier to scale your business.

4. Tax Benefits and Government Schemes

Registered companies in India enjoy several tax deductions and exemptions under the Income Tax Act. They can also benefit from initiatives like Startup India, which provide tax holidays, easier compliance, and faster access to funding. These benefits can significantly reduce operating costs in the initial years of business.

5. Brand Credibility and Trust

A registered company enjoys higher credibility in the market. Clients, suppliers, and global partners take registered businesses more seriously because they reflect transparency and accountability. This credibility can be the deciding factor when securing contracts, building partnerships, or expanding into new markets.

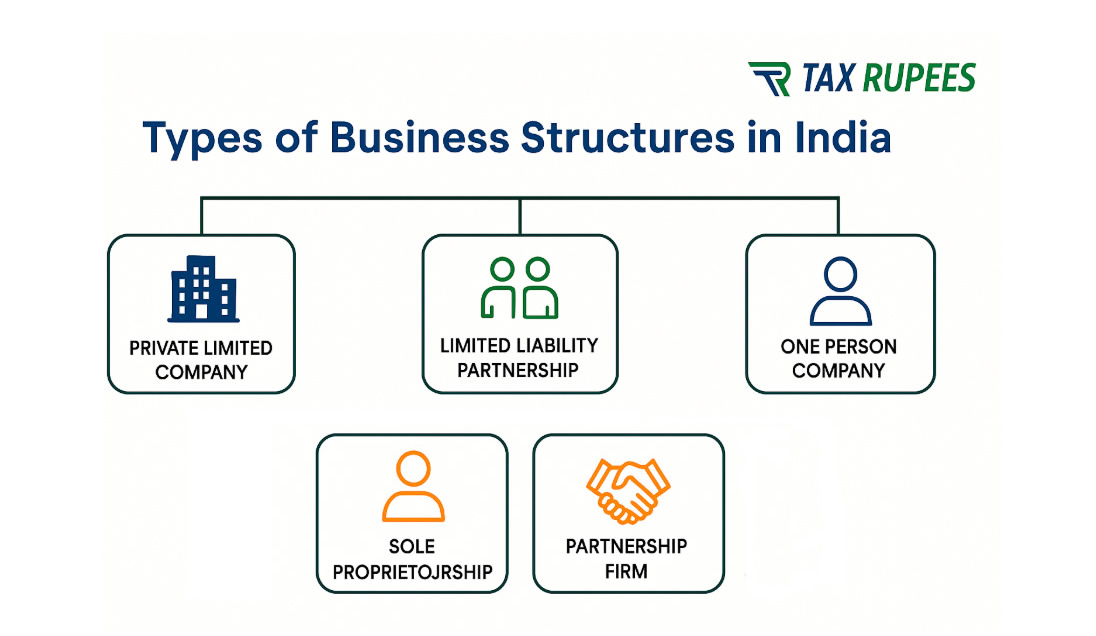

Types of Business Structures in India

When starting a business in India, one of the most important decisions you need to make is choosing the right business structure. The structure you select will determine how your business is taxed, how much liability you hold, how much compliance you need to follow, and even how easily you can raise funding in the future.

India offers several types of business entities. Each has its own advantages and limitations, and the “best” structure depends on your business goals, scale, and resources. Let’s go through each in detail:

1. Private Limited Company (Pvt Ltd)

A Private Limited Company is the most popular structure in India, especially among startups and businesses looking to raise capital.

Key Features:

- Requires a minimum of 2 directors and 2 shareholders (can be the same individuals).

- Treated as a separate legal entity.

- Limited liability for shareholders.

- High compliance requirements, including annual ROC filings, board meetings, and audits.

Advantages:

- Separate legal identity and strong credibility.

- Limited liability for owners.

- Eligible for venture capital, angel funding, and bank loans.

- Can easily scale and expand globally.

Limitations:

- Higher compliance and costs compared to other structures.

- Annual audit mandatory.

Best for: Startups, scaling businesses, and entrepreneurs who plan to raise external investment. Also Read - How to Register Private Limited Company

2. Limited Liability Partnership (LLP)

Introduced under the LLP Act, 2008, the LLP is a hybrid between a partnership firm and a company.

Key Features:

- Requires a minimum of 2 partners (no limit on maximum).

- Partners’ liability is limited to their contribution.

- Separate legal entity from partners.

- Annual compliance is lower than Pvt Ltd but more than partnership firms.

Advantages:

- Lower compliance compared to Pvt Ltd.

- Flexible ownership and management structure.

- Limited liability for partners.

- No restrictions on profit distribution.

Limitations:

- Cannot raise venture capital or issue shares.

- Still requires ROC filings.

Best for: Small and medium-sized businesses, service providers, and professionals like CAs, doctors, and lawyers. Also Read - How to register LLP

3. One Person Company (OPC)

The One Person Company was introduced in 2013 to encourage solo entrepreneurs. It allows a single person to enjoy the benefits of a company without needing co-founders.

Key Features:

- Can be formed by just one person as both director and shareholder.

- Separate legal entity with limited liability.

- Mandatory to appoint a nominee in case of death/incapacity of owner.

- Must convert into Pvt Ltd if turnover exceeds ₹2 crore.

Advantages:

- Limited liability with sole ownership.

- Better credibility than proprietorship.

- Suitable for freelancers, consultants, and small businesses.

Limitations:

- Limited scope for fundraising.

- Cannot have more than one shareholder.

Best for: Solo entrepreneurs who want a corporate structure. Also Read - One Person Company in India: Guide for Entrepreneurs

4. Partnership Firm

A Partnership Firm is one of the oldest forms of business structure in India, governed by the Partnership Act, 1932.

Key Features:

- Requires at least 2 partners (maximum 50).

- Partnership deed defines rights and responsibilities.

- Not a separate legal entity; partners have unlimited liability.

Advantages:

- Easy to form and inexpensive.

- Minimal compliance compared to LLP or Pvt Ltd.

- Flexibility in management.

Limitations:

- Partners’ personal assets are at risk due to unlimited liability.

- Difficult to raise loans or attract investors.

Best for: Family businesses, small traders, or businesses with limited scope. Also Read - Step-by-Step Guide to form a Partnership Firm

5. Sole Proprietorship

A Sole Proprietorship is the simplest and cheapest business form. It is owned and managed by a single person.

Key Features:

- Not a separate legal entity.

- Unlimited liability of the owner.

- Very low compliance requirements.

Advantages:

- Easy to start with minimal cost.

- Complete control by owner.

- No need for complex registration processes.

Limitations:

- Unlimited liability puts personal assets at risk.

- No credibility with investors or banks.

- Business ends with the death of the owner.

Best for: Freelancers, shopkeepers, and self-employed individuals with very small businesses. Also Read - How to Register a Sole Proprietorship

6. Other Structures (Special Mentions)

- Section 8 Company: Non-profit organizations (NGOs, charitable trusts) formed for social objectives. Profits must be reinvested in the mission.

- Public Limited Company: Suitable for large-scale businesses planning to raise money through IPOs. Requires minimum 3 directors and 7 shareholders.

- Producer Company: Special structure for farmers and agricultural producers.

Detailed Comparison of Business Structures

| Factor | Pvt Ltd Company | LLP | OPC | Partnership Firm | Proprietorship |

|---|---|---|---|---|---|

| Minimum Members | 2 Directors, 2 Shareholders | 2 Partners | 1 Person | 2 Partners | 1 Person |

| Legal Entity Status | Separate | Separate | Separate | Not Separate | Not Separate |

| Liability | Limited | Limited | Limited | Unlimited | Unlimited |

| Compliance Level | High | Medium | Medium | Low | Very Low |

| Taxation | 22% + surcharge | 30% slab | 22% corporate tax | Personal rate | Personal rate |

| Fundraising Potential | High | Low | Low | Very Low | None |

| Best For | Startups, scale | Professionals | Solo founders | Family biz, SMEs | Freelancers, traders |

Which Business Structure Should You Choose?

- If you are building a startup with funding potential, go for Private Limited Company.

- If you are a small professional firm or service provider, LLP works best.

- If you are a solo entrepreneur wanting credibility, OPC is a good option.

- If you are a small trader or family-run business, Partnership Firm may work.

- For freelancers and very small businesses, Proprietorship is the simplest choice.

Step-by-Step Company Registration Process in India

Thanks to the Ministry of Corporate Affairs (MCA), company registration in India has become almost fully digital. The entire process is handled online through the SPICe+ form (Simplified Proforma for Incorporating a Company Electronically Plus). This integrated form allows entrepreneurs to:

- Reserve the company name

- Apply for incorporation

- Allot Director Identification Number (DIN)

- Get PAN & TAN

- Apply for GST registration (optional)

Let’s walk through the registration process step by step:

Step 1: Obtain Digital Signature Certificate (DSC)

Since the entire company registration process is online, the first requirement is a Digital Signature Certificate (DSC) for all proposed directors and subscribers of the company.

- What is DSC?

A DSC is an encrypted digital key that verifies the identity of the holder. It is used to sign electronic forms on the MCA portal. - Who issues DSC?

Licensed Certifying Authorities (CAs) like eMudhra, Sify, or NCode Solutions. - Documents needed:

PAN, Aadhaar, passport photo, email ID, and phone number. - Validity:

Usually 1–2 years.

Pro tip: Apply for DSC well in advance because without it, you cannot proceed with MCA filings.

Step 2: Apply for Director Identification Number (DIN)

A DIN is a unique 8-digit identification number allotted to every person who wishes to become a director of a company in India.

- How to apply?

- Earlier, DIN was applied separately using Form DIR-3.

- Now, you can apply for DIN directly while filing the SPICe+ form.

- Documents required:

Identity proof (PAN for Indian nationals), address proof, and a passport photo.

If directors already have a DIN, you can directly use the same while incorporating the company.

Step 3: Reserve Company Name

Selecting the right name for your company is critical. The name must comply with MCA’s naming guidelines and should not be identical or similar to any existing trademark.

- How to apply?

- File Part A of the SPICe+ form on the MCA portal.

- You can apply for two name options at a time.

- Guidelines for name approval:

- Name should reflect the business activity.

- Must end with “Private Limited” or “Limited Liability Partnership” depending on structure.

- Should not violate trademarks.

- Avoid words like "Government", "National", "Bank" unless authorized.

- Processing time:

Usually 2–3 working days.

Pro tip: Do a quick search on MCA’s company name database and the IP India trademark database before applying.

Step 4: Draft Memorandum of Association (MOA) and Articles of Association (AOA)

Two important documents need to be prepared before filing incorporation:

- Memorandum of Association (MOA): Defines the objectives and scope of activities of the company.

- Articles of Association (AOA): Defines internal rules of governance, including appointment of directors, shareholding, and voting rights.

MCA provides e-MOA and e-AOA templates that can be digitally signed by subscribers.

Step 5: File SPICe+ Form (Part B)

This is the most crucial step in the registration process. The SPICe+ form is a single window for all incorporation services.

- Details covered in SPICe+ form:

- Company details (name, registered office, capital)

- Director and shareholder details

- DIN application (if new)

- PAN and TAN application

- GST registration (optional)

- Supporting forms:

- AGILE-PRO-S: For GST, EPFO, ESIC, bank account opening.

- INC-9: Declaration by directors/subscribers.

- Fees payable:

Government fees + stamp duty (varies by state and share capital).

Step 6: Certificate of Incorporation (CoI)

Once the Registrar of Companies (ROC) verifies the SPICe+ application and documents, the Certificate of Incorporation (CoI) is issued.

- What does CoI contain?

- Company’s Corporate Identity Number (CIN)

- Date of incorporation

- PAN and TAN details

With this certificate, your company officially comes into existence.

Step 7: Apply for PAN, TAN, and Bank Account

The SPICe+ form automatically generates PAN and TAN. Once you receive the CoI, you can:

- Apply for a current account in any bank.

- Start business transactions.

Most banks now require the CoI, PAN, and a board resolution to open an account.

Step 8: Apply for GST Registration (if applicable)

If your company’s turnover is expected to exceed ₹40 lakhs (₹20 lakhs for services), you must apply for GST registration.

- You can apply via the AGILE-PRO-S form along with incorporation.

- Once approved, GSTIN will be issued.

Timeline for Company Registration

| Step | Estimated Time |

| DSC Application | 1–2 days |

| Name Approval | 2–3 days |

| Filing SPICe+ + Verification | 3–5 days |

| Certificate of Incorporation | 7–10 days |

If documents are in order, the entire process can be completed within 7–10 working days.

Flowchart: Company Registration Process

Business Idea → DSC → DIN → Name Approval → MOA/AOA → SPICe+ Filing → CoI → PAN/TAN → GST → Bank Account

Practical ExampleCase Study: Rajesh and Anita want to start an e-commerce business selling handmade products. They choose a Private Limited Company structure because they plan to raise investment in the future.

- They obtain DSCs → Apply for DIN → Reserve name “CraftBay Private Limited.”

- File MOA & AOA → Submit SPICe+ form → Receive CoI in 9 working days.

- With CoI, they open a bank account, apply for GST, and launch their brand online.

Result: Within 2 weeks, their business is legally registered and investor-ready.

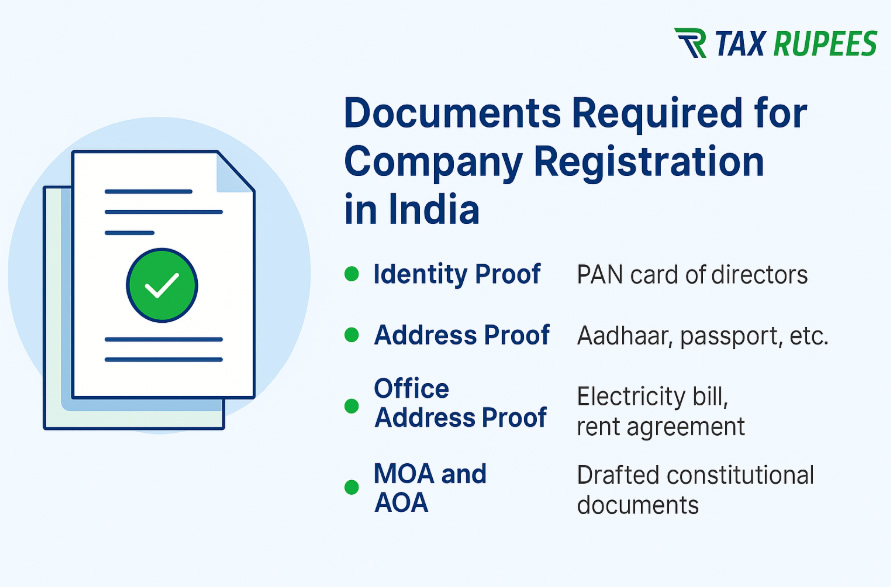

Documents Required for Company Registration in India

To register a company in India, you need to submit a set of identity proofs, address proofs, and business-related documents. The MCA portal only accepts scanned copies, which must be self-attested and digitally signed using the DSC (Digital Signature Certificate) of the directors/shareholders.

Here’s a complete checklist:

1. Identity Proof of Directors and Shareholders

Every director and shareholder must provide valid identity documents.

- PAN Card (mandatory for Indian nationals)

- Passport (mandatory for foreign nationals and NRIs)

Note: For NRIs/foreigners, documents must be notarized and apostilled as per international norms.

2. Address Proof of Directors and Shareholders

Along with identity proof, each director/shareholder must provide address proof that is not older than 2–3 months. Acceptable documents include:

- Aadhaar Card

- Voter ID

- Passport

- Driving License

- Bank statement

- Utility bill (electricity, telephone, gas bill)

3. Passport-Sized Photographs

Recent color passport-size photos of all directors and shareholders are required. These are uploaded digitally on the MCA portal.

4. Proof of Registered Office Address

Every company in India must have a registered office address for communication with government authorities. Documents required are:

- Recent electricity bill, water bill, or property tax receipt (not older than 2 months).

- If rented premises: Rent agreement + No Objection Certificate (NOC) from the landlord.

- If owned property: Sale deed or ownership papers.

Even your residential property can be used as the registered office with proper documentation.

5. Utility Bills and NOC

- Utility bills (electricity, gas, or telephone) are mandatory to establish proof of office.

- If the office is rented, a No Objection Certificate (NOC) from the landlord must clearly state that the premises can be used as the registered office of the company.

6. Company-Specific Documents

- Draft Memorandum of Association (MOA) – states the objectives of the company.

- Draft Articles of Association (AOA) – defines internal management rules.

- Digital Signature Certificates (DSC) of directors and shareholders.

Pro Tip

- Ensure all documents are clear, scanned in color, and in PDF format.

- Address proofs must match the permanent address of directors.

- Keep documents handy because incomplete or mismatched proofs are the most common reason for delays in company registration.

Cost of Company Registration in India

The cost of registering a company in India depends on the business structure you choose, the state of incorporation, and the authorized share capital. Broadly, costs are divided into two parts:

- Government Fees & Stamp Duty – Paid to the Ministry of Corporate Affairs (MCA) and Registrar of Companies (ROC). This varies by state and capital.

- Professional Charges – Fees paid to Chartered Accountants (CAs), Company Secretaries (CS), or service providers who handle documentation, filing, and compliance on your behalf.

Average Cost Breakdown

| Business Structure | Govt. Fees (Approx.) | Professional Fees | Total Estimated Cost |

| Private Limited | ₹7,000 – ₹10,000 | ₹8,000 – ₹12,000 | ₹15,000 – ₹20,000 |

| LLP | ₹5,000 – ₹7,000 | ₹5,000 – ₹8,000 | ₹10,000 – ₹15,000 |

| OPC | ₹6,000 – ₹8,000 | ₹6,000 – ₹8,000 | ₹12,000 – ₹15,000 |

| Partnership Firm | ₹1,000 – ₹2,000 | ₹2,000 – ₹5,000 | ₹3,000 – ₹7,000 |

| Proprietorship | Minimal (0 – ₹1,000) | ₹2,000 – ₹3,000 | ₹2,000 – ₹4,000 |

Key Points to Remember

- Authorized Capital Impact: If your authorized share capital is higher than ₹1 lakh, the govt. fee will increase.

- State-Wise Variation: Stamp duty charges vary across states (e.g., Delhi vs Maharashtra).

- Mandatory DSC & DIN: DSC (₹800–₹1,200 each) and DIN application costs are part of the total registration fee.

- Annual Compliance Costs: Apart from registration, you must budget for yearly compliance (ROC filings, audit, GST, etc.), which typically ranges from ₹10,000 – ₹20,000 per year for Pvt Ltd/LLP.

Post-Registration Compliance in India

Getting your Certificate of Incorporation (CoI) is just the beginning. Once your company is legally registered, you must comply with a set of ongoing rules and filings to stay legally valid. Ignoring compliance can result in penalties, late fees, or even strike-off by the Registrar of Companies (ROC).

Here’s a breakdown of the key compliances after company registration:

1. Opening a Bank Account

- After incorporation, you must open a current account in the company’s name.

- Banks will ask for the CoI, PAN, TAN, and a board resolution.

- All business transactions must go through this account to maintain transparency.

2. PAN, TAN, and GST Registration

- PAN and TAN are allotted automatically through SPICe+ incorporation.

- If your turnover exceeds ₹40 lakh (₹20 lakh for service businesses), you must obtain GST registration.

- If you’re into exports, you may also need an Import Export Code (IEC).

3. Statutory Registers and Records

Companies are required to maintain certain registers, such as:

- Register of members

- Register of directors

- Register of charges

- Minutes of board meetings

These records must be updated regularly and kept at the registered office.

4. Annual Compliance Filings

Depending on your business structure, you need to file the following every year:

- Private Limited Companies & OPCs: Annual ROC filings (Form AOC-4, MGT-7), board meetings, statutory audit.

- LLPs: Annual return filing (Form 11) and Statement of Accounts (Form 8).

- Partnerships/Proprietorships: ITR filing based on income tax slabs.

5. Income Tax and Other Returns

- All businesses must file Income Tax Returns (ITR) every year.

- TDS compliance applies if you have employees or make specified payments.

- GST-registered companies must file monthly/quarterly returns.

6. Additional Compliances

- Shops & Establishment Act registration (if applicable).

- EPFO and ESIC registration if you employ more than 10 workers.

- Regular bookkeeping and accounting.

Pro Tip: Compliance is an ongoing responsibility. Hiring a CA/CS or outsourcing compliance management helps avoid penalties and keeps your company in good legal standing.

How TaxRupees Can Help

Starting a company in India can feel overwhelming because of the multiple forms, documentation, and compliance requirements involved. Even a small mistake during filing can lead to delays, rejections, or penalties. That’s where TaxRupees makes a difference.

At TaxRupees, our goal is to simplify the process for entrepreneurs, startups, and small business owners so that you can focus on building your business while we handle the legal and compliance side.

Here’s how we can help you:

- Choosing the Right Structure – Our experts guide you in selecting the most suitable business structure (Pvt Ltd, LLP, OPC, or others) based on your goals, budget, and compliance needs.

- End-to-End MCA Filings – From DSC/DIN application to SPICe+ filing and name approval, we manage the entire registration process seamlessly through the MCA portal.

- Compliance Assurance – We ensure your company remains fully compliant with ROC annual filings, GST registration/returns, and Income Tax rules.

- Startup-Friendly Packages – Affordable, transparent pricing tailored for early-stage founders, without hidden costs.

By partnering with TaxRupees, you don’t just register a company. You set up your business for smooth, compliant, and growth-ready operations.

Register your company hassle-free with TaxRupees today and take the first step toward building your dream business.

Get Your Company Registered

Contact Tax Rupees for all your Business Needs

FAQs

1. Can I register a company from home?

Yes, you don’t need to visit any office physically. The entire company registration process in India is 100% online through the Ministry of Corporate Affairs (MCA) portal. You can submit documents, pay fees, and track your application digitally.

2. How much time does it take?

On average, it takes about 7–10 working days to register a company, provided all the documents are correct and verified on time. Sometimes delays may occur if there are discrepancies in the application or additional approvals are required.

3. What is the minimum capital required?

There is no minimum capital requirement for starting a company in India. You can even start with a capital of ₹1. However, it’s advisable to keep a practical capital amount that reflects your business needs and operations.

4. Can NRIs or foreigners register a company in India?

Yes, both Non-Resident Indians (NRIs) and foreign nationals can register a company in India. They need to follow the Foreign Direct Investment (FDI) guidelines and may also require approval from the Reserve Bank of India (RBI) depending on the sector.

5. Is GST compulsory after registration?

GST (Goods & Services Tax) is not compulsory immediately after registering a company. You only need to apply for GST if your business turnover exceeds ₹40 lakhs in case of goods, or ₹20 lakhs in case of services. Voluntary registration is also possible if you want to claim input tax credit.

6. What happens if I don’t file annual returns?

If a company fails to file its annual returns with MCA, it attracts heavy penalties and late fees. Persistent non-compliance may also lead to your company being struck off from the MCA records, which means it will no longer exist legally.

7. Can I convert my OPC to Pvt Ltd?

Yes, you can convert your One Person Company (OPC) into a Private Limited Company. In fact, this conversion becomes mandatory once your company’s turnover crosses ₹2 crore or its paid-up capital exceeds ₹50 lakh.

8. Can a company name be changed later?

Yes, you can change your company’s name even after incorporation. The process requires board and shareholder approval and filing the form INC-24 with MCA along with the required fees. Once approved, the new name will appear in all official records.

9. Do I need a CA/CS to register?

Technically, you can register a company yourself through the MCA portal without hiring a Chartered Accountant (CA) or Company Secretary (CS). However, since the process involves legal compliance and document preparation, it’s highly recommended to seek professional help to avoid mistakes and delays.

Conclusion

Registering a company in India is now faster and easier thanks to the MCA’s digital initiatives. Whether you are a solo entrepreneur, a small business owner, or a startup founder aiming for investment, company registration gives you legal protection, credibility, and access to growth opportunities.

With the right structure, proper documents, and professional guidance, your company can be registered in less than two weeks.

If you are ready to start your business journey, let TaxRupees handle the process while you focus on building your dream.